By John Boyce

In March and April, the bloodstock sales world stood on the precipice, or so it seemed, as the Inglis Easter Yearling Sale–the first major international auction to confront the social upheaval of COVID-19–was put under severe pressure. In the event, team Inglis rose to the challenge and showed a potential way forward for other sales houses with its innovative virtual sale. It didn't, however, escape completely unscathed, and trepidation remained high for those with horses to sell all over the Northern Hemisphere.

Six months on, we can now report that the sales went ahead–not all in their chosen venues and dates and not all with their original lineups–but horses were sold nonetheless, cash flowed so that bills will get paid and future investment funds will be found.

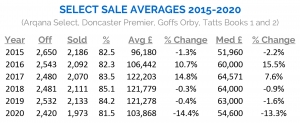

Remarkably, Europe's five big yearling auctions–Arqana, Doncaster Premier, Goffs Orby and Tatts Books 1 and 2–ended up with an average price just over 14% behind where it was 12 months ago. In essence, prices in 2020 are still ahead of where they were as recently as 2015. It's a truly miraculous turn of events considering what we thought we faced six months ago.

It wasn't good news for everyone, though. Confidence didn't really return until Tattersalls staged their annual yearling sale during the first two full weeks in October. By then, both the Goffs Orby and Doncaster Premier Sales–shorn of some of their big investors and with the distinct disadvantage of having to change venue and open the calendar, respectively–had suffered sizeable setbacks, their averages shrinking by 35% and 27% respectively, while their clearance rates fell by about five percentage points. And although Arqana didn't suffer quite so badly–its average 11% shy of last year's figure–it was really Tattersalls that saved the 2020 European yearling market. Its Book 1 provided a gloss at the elite end, but it was Book 2 that really led the recovery that spilled over into Book 3.

Tattersall Book 1 was the place to sell if your yearling was among the top 45 to 50 at the sale. For this group, the average was down only 3%, but for the next two sets of 45-50 yearlings the average fell away markedly by 19% and 25%, respectively. In fact, it was so tough lower down the order at Book 1 that there will be plenty who wished their yearling had been in Book 2. For starters, Book 2 recorded a higher clearance rate–85.3% to 84.9%–than last year. Then there's the fact that its top three deciles (225 yearlings) were down by only 4%, 1% and 6%, respectively. And for the rest of the sale, reversals in average were for the most part kept below 10% giving Book 2 an overall average just 3% behind last year's sale.

But we cannot just talk about the elite market. So many commercial yearlings are produced these days that many spill over into other less lucrative auctions. It is interesting to note for instance that in a normal year 76% of all yearlings sold by sub-20k stallions in Europe are auctioned outside the five main sales. Even the 20k-plus stallions have significant numbers (31%) of their yearlings sold at the non-elite sales. No one yet knows what the final implications for the yearling and nominations market will be. It looks like we will have to wait until January before we get a complete and accurate sales picture.

Even before COVID-19 arrived on the scene, there was pressure on profitability building within the European yearling market. It's not that stallion studs have individually been hiking fees recently; it's the fact that the number of high-priced stallions on European rosters in the past six years is at an all-time high. Ten years ago only 13 of the top 30 stallions in Britain and Ireland assessed by book quality stood at £20,000/€20,000 or more. By 2019 that number had risen to 22 out of 30. The cheapest fee of the top 30 stallions in 2009 was £15,000 and by 2019 it had risen to £30,000.

To illustrate the point, we can use the elite European Sales. In 2018, 2,111 yearlings were sold at these five sales and 67% made enough to cover their sire's advertised fee, plus £20,000 in production costs. A year later, the 2,133 yearlings sold included 65% that were profitable by the same criteria – down two percentage points. This year, whilst it is excellent news that as many as 1,973 found new homes from the five sales, the margins were squeezed so much that only 58% cleared the advertised-fee-plus-£20k hurdle. We can, of course, lay most of the blame for this seven-point drop on the COVID-19 disruption, but there's a good chance that the number would have been down anyway.

There have been precious few silver linings to the COVID-19 cloud. For the bloodstock industry, it will surely hasten a fundamental review of the supply and demand of commercial young stock over the next few years, with implications for everyone in connected markets.

Not a subscriber? Click here to sign up for the daily PDF or alerts.