By Dean Towers

For the past few years, the National Thoroughbred Racing Association (NTRA) has been lobbying for changes to the tax code on behalf of racetracks and betting customers. Since the late 1960's, single wagers paying over 300-1 were reported to be taxed, and bets that pay over $5,000 were subject to withholding.

The NTRA believes that (with inflation and the explosion of exotic wagering) this is unfair, and they've drafted a proposal to modernize the system. They are now in the home-stretch of this effort, and (so far) with little resistance, there's a strong chance new rules will be enacted sometime in 2017.

When I speak to some in the industry, or scan social media, this subject seems to not get much attention. Now, I don't expect accounting jargon to light up the masses like an Arrogate charge in Dubai, but still, the reaction to this has been somewhat muted. In my view, it should not be.

Betting handle, in the absence of alternate gaming on-site, is what makes most everything go. Purses, backstretch monies, horse retirement, taxes, and myriad other things are taken directly out of betting handle in states like yours. The more handle, the more money.

There are many determinants to betting handle's growth, or shrinkage–the takeout rate, the number of races held, field size, distribution of the product, etc–but all of those, and others, rely on (or are related to) the size of aggregate customer bankrolls.

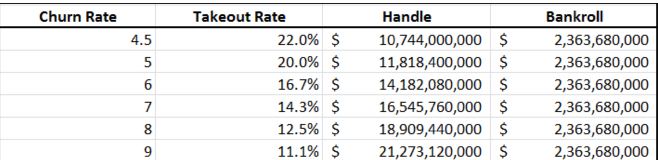

According to the Jockey Club Fact Book, about $10.74B was bet in the US last year on Thoroughbred racing. Using a blended takeout rate of 22% (in the absence of rebating), about $2.3B was held for racing revenue. This $2.3B was in betting accounts, brought to the track and simo-centers by customers in 2016, and it was rolled over about 4.5 times (the churn rate).

For reference and comparison, the chart below (data courtesy of the International Federation of Racing) shows churn rates and betting bankrolls for various countries with 2015 data (2016 for the US).

Despite an often heard narrative that people love to bet racing in Hong Kong, Australia or Ireland (which is true), it's important to know that aggregate betting bankrolls in the US are probably higher than in all of these countries. The difference is the lower takeout, which enable customers to roll over more of their bankrolls.

Now, racing in the US can theoretically increase handle by decreasing takeout rates–horse racing bettors are creatures of habit, and bet set percentages of what's available for them to bet (see table). Peer reviewed studies also postulate that if racing makes itself a better bet it will attract more money and bankrolls will grow. But increasing a churn rate doesn't directly increase bettor's bankrolls.

For our purposes, though, via the NTRA's tax proposals, the bankroll number will increase–not theoretically but in reality– because money is not withheld that was withheld. In the chart below I have estimated a base bankroll increase of 0.5%. I also increased the churn rate modestly to a 5 because bigger players with bigger bankrolls have a higher churn rate (through takeout breaks). In 2007 in Hong Kong, for example, a new 10% rebate on tickets over $US1,200 resulted in a boost in revenue where 60% of the gross handle gain was generated from these higher value players. It was not linear.

In addition, for players who have long left betting the sport because of bankroll degradation through these tax policies, it is likely at least some of them may return to bet a few dollars on the horses. Getting back the full amount of a 12% takeout pick 5 score makes the game a lot more fun than it used to be, and in a game with a tagline “you can beat a race but can't beat the races,” it chips away at a negative narrative.

Even with these potential synergies, and results, perhaps the potential handle increases in our handy table don't “wow” you. That's perfectly understandable; handle isn't doubling overnight. But, for an industry that has seen falling handle numbers most years in the 21st century, it's very positive.

As well, from a business perspective, I think it's important to look at this in the context of the “flywheel”.

In Jim Collins' best-selling business book, Good to Great: Why Some Companies Make the Leap… and Others Don't, the author mined data of 1,435 legacy companies and looked for characteristics that were positive for their long-term growth. Time and time again he found that success didn't come from a light bulb moment; growth came by incremental improvements. He likened it to a flywheel. A static wheel takes great effort to move. The first two, or three, or four pushes are incredibly difficult, but by the eighth and tenth and twelfth, the wheel is easier to move.

“The flywheel image captures the overall feel of what it was like inside the companies as they went from good to great. There was no single defining action, no grand program, no one killer innovation, no solitary lucky break, no wrenching revolution. Good to great comes about by a cumulative process–step by step, action by action, decision by decision, turn by turn of the flywheel,” he wrote.

Over the last decade, customers have seen their bankrolls degraded through higher takeout, new source market fees, increasing signal fees, jackpot bets and myriad other policy changes. By 2018, there's a chance they'll see an increase. For them it means more enjoyment in the game, because their bankrolls can last longer. For the business of racing, a happy customer enjoying themselves stays in the racing ecosystem; some generating ongoing revenue for a lifetime. I applaud what the NTRA has undertaken and is about to accomplish. When you increase customer bankrolls good things can happen–for everyone.

Dean Towers has been a Board Member of the Horseplayers Association of North America since 2008, and has presented at numerous wagering conferences across North America.

Not a subscriber? Click here to sign up for the daily PDF or alerts.